How to Finance a Custom Home Build in Phoenix: What You Need to Know

Financing a custom home build in Phoenix works differently from financing a home purchase. There is no existing structure for the lender to appraise. There is no seller. The asset the bank is lending against is a set of plans, a licensed contractor, and a piece of land. Understanding how construction financing works – and what lenders require from your builder – before you start is the difference between a smooth project and a financing-caused delay that sets construction back three to four months.

Quick Answer: Most Phoenix custom home builds are financed through a construction-to-permanent loan, which converts to a traditional mortgage at completion. Lenders require a licensed, insured General Contractor with verifiable financials, a fixed-price or maximum-price contract, stamped architectural plans, and a verified draw schedule. Prolific Builders works directly with construction lenders, provides all required documentation, and manages the draw process from groundbreaking through certificate of occupancy. Arizona ROC License #356246. BuildZoom Score 100. Call (480) 972-3000.

The Two Main Ways to Finance a Custom Home Build

Option 1: Construction-to-Permanent Loan (One-Time Close)

A construction-to-permanent loan funds the build in stages through a draw schedule, then automatically converts to a standard mortgage when the certificate of occupancy is issued. You apply once, close once, and pay one set of closing costs. During construction, you typically pay interest only on the draws that have been released. At conversion, the loan becomes a 15- or 30-year mortgage at a rate locked at origination or at conversion, depending on lender terms.

This is the most common financing structure for Phoenix custom builds because it eliminates the double-closing cost of a standalone construction loan followed by a purchase mortgage. The single qualification process also reduces underwriting complexity.

Option 2: Standalone Construction Loan Plus Permanent Mortgage (Two-Time Close)

A standalone construction loan is a short-term loan – typically 12 to 18 months – that funds the build and is paid off at completion with proceeds from a new permanent mortgage. You close twice, pay two sets of closing costs, and qualify twice. The upside is that you can shop for the best permanent mortgage rate at the time construction is complete rather than locking before the build begins. In a declining rate environment, this flexibility has real value. In a stable or rising rate environment, the convenience of the one-time close typically wins.

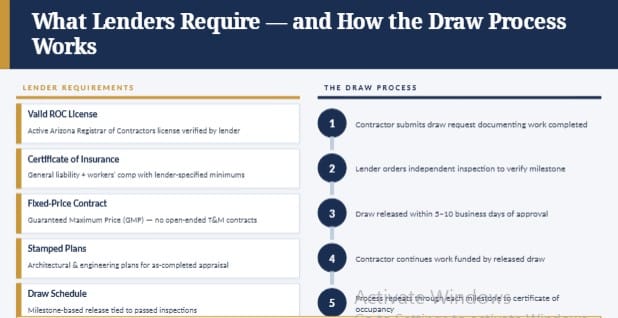

What Lenders Require From Your Builder

Construction lenders do not fund builds with unlicensed or unvetted contractors. Before approving a construction loan, the lender’s underwriting team will review your builder’s qualifications. Understanding what they look for helps you choose a contractor who will not stall your financing approval.

Valid contractor license. Lenders verify that your General Contractor holds an active Arizona ROC license. The Arizona Registrar of Contractors license lookup confirms license status, license type, bond status, and complaint history. Victor Torres at Prolific Builders holds ROC License #356246 – dual commercial and residential General Contractor.

Certificate of insurance. Lenders require your contractor to carry general liability insurance and workers’ compensation coverage with minimum limits specified in the loan agreement. Prolific Builders provides certificates of insurance directly to lenders as part of the documentation package.

Fixed-price or maximum-price contract. Open-ended time-and-materials contracts create unlimited lender exposure. Most construction lenders require a fixed-price or guaranteed maximum price (GMP) contract that caps the total construction cost and identifies what is included. This is why vague “estimate plus overages” contracts from undercapitalized contractors create financing problems even when the contractor is competent.

Stamped architectural and engineering plans. Lenders commission an independent appraisal of the proposed home based on the plans, the specifications, and comparable sales. The appraiser issues an “as-completed value” – the estimated market value of the finished home. If the as-completed appraisal does not support the loan amount, the deal does not work, regardless of how good the plans are. Plans must be detailed enough for the appraiser to assess finish quality accurately.

Draw a schedule and a construction timeline. The lender structures loan advances around a milestone-based draw schedule tied to inspections. Typical draws release at foundation completion, framing, rough mechanicals, drywall, and completion. Your builder must complete and pass inspection at each milestone before the next draw is released.

How the Draw Process Works

Construction loans do not hand over the full loan amount on day one. Funds are released in stages as construction progresses and inspections are passed. Here is how the draw cycle typically works:

- Contractor submits a draw request to the lender documenting work completed to date and the percentage of project completion.

- Lender orders an inspection by an independent inspector or appraiser who verifies that the claimed work is complete and meets plan specifications.

- Lender releases the draw directly to the contractor (or to a title company disbursement account) within five to ten business days of inspection approval.

- Contractor continues work into the next phase, funded by the released draw.

- Process repeats through each milestone until the certificate of occupancy is issued and the final draw is released.

Cash flow management during the draw cycle is one of the clearest advantages of working with an established, well-capitalized builder. A contractor who cannot bridge between draw releases – who needs the next draw before completing the prior phase – introduces schedule risk that has nothing to do with workmanship.

Land Financing and Lot Equity

If you own the lot free and clear, most lenders count the land value as part of your equity contribution toward the construction loan, reducing the cash down payment required. If you are purchasing land simultaneously with financing the build, you will need either a lot loan (typically requiring 20-30% down) or a combined land-and-construction loan available from some portfolio lenders.

In the Phoenix metro, lot prices vary widely by location, size, and utilities. Goodyear, Surprise, and Buckeye lots in master-planned communities with utilities to the pad are currently ranging from $120,000 to $250,000 for standard custom home lots. Infill lots in Scottsdale, Paradise Valley, and central Phoenix command significantly higher prices and often require more complex site preparation.

What to Budget Beyond the Construction Loan

Construction financing covers the cost of building. It does not cover everything you will spend before occupancy. Budget for the following out-of-pocket costs in addition to your construction loan down payment:

- Loan origination fees and closing costs: Typically 1-2% of the loan amount

- Interest reserve: Some lenders require an interest reserve funded at closing to cover interest payments during construction without requiring monthly out-of-pocket payments

- Architectural and engineering fees: If not included in the builder’s design-build contract

- Permit fees: City of Phoenix permit fees on a 3,000 sq ft custom home typically run $8,000 – $15,000, depending on scope and municipality

- Landscaping: Often not included in construction contracts

- Window treatments, appliances, and non-built-in furnishings: Rarely included

- HOA initiation fees: If applicable in the community

Why Builder Documentation Quality Affects Your Financing Timeline

Construction loan underwriting moves at the speed of the documentation your builder provides. Lenders who are waiting for a contractor to produce a compliant fixed-price contract, updated insurance certificates, or a coherent draw schedule cannot advance the loan to approval regardless of your personal creditworthiness.

Prolific Builders has prepared documentation packages for construction lenders on every project in its portfolio. The fixed-price contract, insurance certificates, ROC license documentation, stamped plans, and draw schedule are standard deliverables – not items that need to be assembled after a lender request. This documentation readiness is part of why Prolific builds consistently to schedule and why lenders approve draws without delay.

ROC License #356246. BuildZoom Score 100. Open-book budgeting on every project. No contract signed until you approve the line-item estimate.

“Bathroom renovation turned out even better than we imagined.” – Cindy Coombs, Homeowner

Working With a Lender: Where to Start

Not all residential mortgage lenders offer construction loans. The best starting points are local credit unions, community banks, and regional portfolio lenders who hold construction paper in-house rather than selling immediately to secondary market investors. National banks offer construction products in some markets, but their underwriting guidelines are typically more rigid, and their familiarity with Arizona-specific land and construction norms is lower than that of local institutions.

When interviewing construction lenders, ask specifically: Do you offer one-time close construction-to-permanent loans? What is your typical draw inspection turnaround time? What are your documentation requirements for the general contractor? What is your minimum down payment for a construction loan with owned land versus purchased land?

Prolific Builders can provide a list of construction lenders currently active in the Phoenix metro market who have approved Prolific projects and are familiar with the company’s documentation package.

Schedule Your Free Consultation

If you are beginning to plan a custom home build in Phoenix and want to understand the financing structure before you commit to a site, Prolific Builders will walk you through the documentation required, the draw schedule structure, and how the design-build contract is structured to satisfy lender requirements.

Arizona ROC #356246. BuildZoom Score 100. No-obligation estimate.

Get My Free Phoenix Build Consultation

Call (480) 972-3000 or visit prolificbuilders.com